Although the mood appears to be waning somewhat, carriers insist they are for the most part optimistic the Canadian freight market can withstand current economic tremors.

The Ontario Trucking Association’s fourth quarter 2015 business conditions survey for the bellwether sector shows that recent freight volume and rate trends – as well as expectations for the future – are generally much more restrained than what’s been expressed in the last several surveys, especially throughout Canadian freight lanes. The weakness of the Canadian economy and unprecedented rising prices for new equipment appear to have caught up with carriers, shifting their current and future outlook more significantly than in the recent past.

Still, 69% of carriers in this 4Q survey say they are “generally optimistic” about the prospects for the trucking industry over the next three months – 16 percent lower than this time last year, but still a large percentage of respondents overall.

Freight Volumes

Freight Volumes

Intra-Ontario and Intra-provincial freight volumes showed early signs of cracking in the 2Q2015 survey and that trend is continuing. Twenty-nine percent of carriers report volume increases in the previous three months, slightly higher than the 25% who saw improvements in the previous survey but still well off the 44% average of carriers who expressed similar sentiments throughout 2014. The 15% who said volumes are decreasing is still relatively low, but is now the highest level in three years of carriers who reported contraction and the first time it’s peaked into double-digit territory since 4Q2013. Fifty-six percent report unchanged volumes.

In comparison to the rest of the country, Ontario freight volumes appear to be holding up fairly well – or at least deflating at a much slower pace that intra-provincial freight demand. Likely due to a sustained economic downturn in the western provinces, only 16% of carriers reported improved volumes in these lanes, which is 20% less than the last quarter and a whopping 43% drop from mid-2014. While the overall majority (60%) still indicate no volume change in this sector, 24% report shrunken volumes – the highest percentage since the midst of the recession in 2009.

Relatedly, with much of the Canadian economy in a slump, northbound U.S. freight volumes also tumbled with just 13% of carriers experiencing improvement (the lowest since 2008) compared to 13% last quarter. Meanwhile, a majority (51%) indicated there was a decrease – up significantly from 14% in 2Q15 and also the highest rate since 2008.

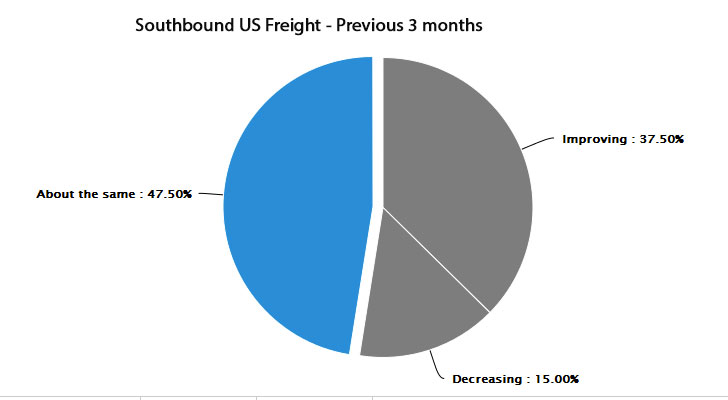

The good news is that on the back of modest US economic growth, carriers who confirmed southbound freight improvements increased to 36% – still half the number of companies who said the same in mid-2014, but better than the 27% rate from the previous 2Q survey.

While signs of a slowing freight environment in that previous 2Q survey didn’t immediately dampen carriers’ prospects for the near future, it definitely appears that back-to-back shrinking freight volumes has begun to temper their expectations. With what has perhaps been a weaker-than-expected ‘peak’ shipping season now coming to a close, only 35% of carriers foresee volumes improving over the next six months – down from the 54% who indicated positive expectations in 2Q2015. Intra-provincially, 24% project improved volumes — half compared to the last survey. The number of people who anticipate contracted volumes are still in the single digits, but previous optimism has shifted towards an expectation of stagnancy as a whopping 69% predict no changes for at least the next six months. Of all the lanes OTA inquires, positive expectations were highest for U.S. southbound volumes. Forty three percent envision increases, down only slightly from the 50% last quarter. As for northbound, positive expectations for the next six months were flat at 18%, while 28% expect decreases – up from 14% in the last OTA survey.

Rates & Capacity

Overall, pricing is either unchanged or softening across the board compared to 2Q15. Within Ontario lanes, 20% expect improvements, down from 33% in the last survey and more than half of 45% who this time last year expected pricing to solidify further. Only 10% of carriers expect rates to actually decrease – although that’s 10% more than in the last three surveys when no carrier suggested the industry should brace for softer rates. As for freight across provincial lines, 68% don’t anticipate any movement, while just 16% said rates will improve, compared to 36% last quarter. Following volumes, rates for U.S. southbound appear to be the most likely to grow, but the 28% of carriers who said so are nearly half of the 56% in 2Q15. For northbound, 23% expect improvements, 28% forecast a pricing fall (the highest level since 2013) and about half (49%) expect no change.

Compressed capacity continues to be an issue keeping a lid on industry expansion, but there are some signs of slackening, at least in the short-term. A majority (56%) of carriers report no change in capacity over the last three months, although only 20% say capacity has tightened, which is the lowest level since 4Q2013. Looking ahead, 20% think capacity will increase, another fifth of respondents expect tightening and 60% don’t think there will be any fluctuation. Carriers still appear committed to adding manpower, however – at least as replacements – with 56% and 51% of carriers saying they plan to hire more owner-ops and company drivers respectively.

Compressed capacity continues to be an issue keeping a lid on industry expansion, but there are some signs of slackening, at least in the short-term. A majority (56%) of carriers report no change in capacity over the last three months, although only 20% say capacity has tightened, which is the lowest level since 4Q2013. Looking ahead, 20% think capacity will increase, another fifth of respondents expect tightening and 60% don’t think there will be any fluctuation. Carriers still appear committed to adding manpower, however – at least as replacements – with 56% and 51% of carriers saying they plan to hire more owner-ops and company drivers respectively.

Carrier Costs

Fleets continue to struggle mightily to keep costs in check. Respondents were nearly unanimous in saying that tractor/engine prices have increased by at least 10%; and, interestingly, 40% of carriers indicated price increases of 20% or higher. Virtually no respondents have ever reported engine-tractor costs higher than 20 percent until this year. While much of this is obviously a result of the widened gap between the CND and US currencies, it’s also possible that with the 2010 EPA emissions mandate now five years old, a larger number of those more expensive, emission-controlled trucks are just starting to make their way into fleets’ replacement cycles.

As carriers compete with each other and industry trades to attract and retain drivers, costs associated with driver and owner-operator wages remain on the upswing. Unchanged from the previous survey, 92% of respondents report wage increases in the 2-5% range with nearly one in 10 carriers say they have hiked pay by 10%.

Top Concerns

UnShakable as the top-rated issue among carriers is the driver shortage, with 40% (down from 50%) ranking it as their number one concern. Alarm over the economy climbed to the second spot (27% said it was their top concern compared to 13% previously). Capacity/rates was the top issue for 23% of carriers.